Are you confused about what it means to be an active participant in a retirement plan? Understanding this term can make a big difference in how you save for your future.

Knowing if you qualify as an active participant affects your contributions, tax benefits, and even your eligibility for other retirement accounts. This article will break down the definition clearly and help you see why it matters for your financial security.

Keep reading to take control of your retirement planning with confidence.

What Is An Active Participant?

Understanding what an active participant is helps you grasp retirement plans better. An active participant is someone who actively joins and contributes to a retirement plan. They play a direct role in building their retirement savings.

Being an active participant means you are currently involved in the retirement plan. This involvement can affect your taxes and benefits. It also influences how much you can contribute and withdraw.

Who Qualifies As An Active Participant?

Anyone who makes contributions to a retirement plan qualifies. This includes employee contributions or employer matching funds. Even those who choose to defer salary into the plan count.

How Participation Affects Retirement Benefits

Active participants often receive better benefits. Their regular contributions grow over time. This growth can lead to a larger retirement fund.

Impact On Tax Rules

Tax rules often depend on active participation. If you are an active participant, certain tax limits apply. These rules may affect your ability to deduct contributions.

Credit: 401kspecialistmag.com

Criteria For Active Participation

Understanding the criteria for active participation in a retirement plan is important. It helps employees know if they qualify for the plan benefits. Employers also use these rules to decide who joins the plan.

Active participation depends on specific factors set by the plan and law. These factors include work hours, employment status, and contributions. Knowing these details can help you plan for a secure future.

Minimum Hours Worked

One key factor is the number of hours worked. Many plans require employees to work a minimum number of hours. This number often ranges from 500 to 1,000 hours per year. Employees below this threshold may not qualify as active participants.

Employment Duration

Another important criterion is how long an employee has worked. Some plans require a minimum period, like one year. This period helps determine if the employee is committed enough to join the plan. Short-term workers may be excluded.

Contributions To The Plan

Contributing to the retirement plan can define active participation. Many plans require employees to make contributions regularly. This shows the employee’s interest in saving for retirement. Some plans also consider employer contributions.

Employment Status

Employment type can affect active participation. Full-time workers often qualify more easily than part-time workers. Temporary or seasonal employees might not meet the criteria. Plan rules vary depending on company policies.

Types Of Retirement Plans Involved

Understanding the types of retirement plans is key to knowing who counts as an active participant. Different plans have different rules for participation and contributions. These plans offer various benefits and limits.

Each retirement plan type has unique features. Knowing these helps employees and employers manage retirement savings better. Here are the main types of retirement plans involved.

401(k) Plans

401(k) plans are popular employer-sponsored retirement savings plans. Employees contribute a portion of their salary before taxes. Employers may match part of the employee’s contribution. Active participation means making contributions or having contributions made on your behalf.

403(b) Plans

403(b) plans are for employees of public schools and some nonprofits. They work like 401(k) plans but have special rules for nonprofit workers. Active participants contribute regularly or receive employer contributions. These plans help employees save on taxes now and in retirement.

Simplified Employee Pension (sep) Plans

SEP plans are for small businesses and self-employed workers. Employers make contributions for employees. Employees do not contribute. Active participation means the employer has made contributions for the employee during the year. These plans have high contribution limits.

Simple Ira Plans

SIMPLE IRAs are for small businesses with fewer than 100 employees. Both employers and employees contribute. Active participation means the employee has made contributions or the employer has contributed. These plans are easier to set up and maintain than 401(k)s.

Defined Benefit Plans

Defined benefit plans promise a specific retirement benefit amount. Employers fund the plan and manage investments. Active participation means being covered by the plan during the year. These plans focus on steady income after retirement.

Credit: manhattan.institute

Impact On Contribution Limits

Being an active participant in a retirement plan affects how much you can contribute each year. Contribution limits set the maximum amount you can put into your retirement accounts. These limits help you save steadily while following tax rules.

Understanding the impact on contribution limits helps you plan your savings better. It shows how your involvement in a plan changes your options for adding money.

What Makes Someone An Active Participant?

An active participant is someone who takes part in an employer-sponsored retirement plan. This includes plans like a 401(k) or a pension. Even small contributions or employer matches count.

Contribution Limits For Active Participants

Active participants have specific contribution limits for their retirement plans. These limits are often lower than those for non-participants. The IRS updates these limits yearly based on inflation.

Effect On Traditional Ira Contributions

Being an active participant can reduce the amount you can deduct from your taxes for traditional IRA contributions. This happens when your income exceeds certain levels. The higher your income, the less you can deduct.

Impact On Roth Ira Eligibility

Active participants with high income might not be able to contribute to a Roth IRA. Roth IRAs have income limits that restrict contributions. This rule encourages saving in other retirement plans instead.

Planning Contributions Wisely

Knowing your status helps you plan your yearly contributions. It avoids exceeding limits and facing penalties. Track your contributions across all retirement accounts to stay within allowed amounts.

Effect On Tax Benefits

Being an active participant in a retirement plan can affect your tax benefits. It may limit your ability to claim certain tax deductions on contributions. Understanding this status helps plan your taxes better.

Being an active participant in a retirement plan changes your tax benefits. It affects how much you can deduct from your taxes each year.

Active participants often have lower limits on tax deductions. This can reduce the amount of money you save on taxes.

The IRS sets rules that limit deductions for active participants. These rules depend on your income and filing status.

Contribution Limits And Tax Deductions

Active participants face stricter limits on contributions. These limits determine how much you can put into your retirement plan tax-free.

If your income is high, your deduction may be smaller or zero. This means you pay taxes on some contributions.

Understanding these limits helps you plan your savings better. It prevents surprises during tax season.

Impact On Traditional Ira Deductions

Active participation affects your ability to deduct traditional IRA contributions. If you participate in a workplace plan, deductions shrink.

High earners may not get any deduction at all. This rule helps balance tax advantages among all taxpayers.

Knowing your status helps you decide if a traditional IRA is right. It also guides you on how much to contribute.

Effect On Roth Ira Eligibility

Active participants still can use Roth IRAs, but income limits apply. Roth contributions are not tax-deductible but grow tax-free.

Higher incomes may reduce or block Roth IRA contributions. This limits your options for tax-free retirement growth.

Checking your active participant status clarifies your Roth IRA choices. It helps you pick the best retirement plan.

Common Misconceptions

Many people misunderstand what an active participant in a retirement plan means. These wrong ideas can cause confusion about eligibility and benefits. Clearing up these common misconceptions helps you make better retirement choices.

What Does “active Participant” Really Mean?

Some think being an active participant means you must contribute money. Others believe just enrolling in a plan counts. The true meaning depends on specific plan rules and IRS guidelines. It usually means you have rights to benefits or contributions during the year.

Active Participation And Eligibility

People often confuse active participation with being eligible for certain tax benefits. Not all participants qualify for tax breaks just by joining. Eligibility depends on your participation status and income limits. Understanding this difference helps avoid surprises during tax season.

Impact On Retirement Contributions

Many assume active participants can always contribute the same amounts. Some plans limit contributions based on participation status. Employers may also have rules that affect how much you can save. Knowing these limits helps plan your savings wisely.

Active Participant And Plan Withdrawals

Another misconception is that active participation affects withdrawal rules. Being active does not change when you can withdraw money. Withdrawal rules follow plan terms and federal laws, not participation status alone.

How To Verify Your Status

Check your retirement plan records to see if you made contributions or received employer matches. Confirm your work hours and salary meet the plan’s active participant rules. This helps determine your status for tax and benefit purposes.

Check Your Retirement Plan Documents

Start by reviewing your retirement plan paperwork. Look for terms like “active participant” or “participation status.” These documents often explain if you qualify as an active participant. Keep an eye on contributions or benefits listed. They show your involvement in the plan.

Ask Your Employer Or Plan Administrator

Contact your employer’s HR department or plan administrator. They can confirm your participation status. They have access to your account details and records. A quick call or email can give clear answers.

Review Your Pay Stubs

Look at your recent pay stubs. Check for deductions related to your retirement plan. Contributions taken out regularly mean you are likely an active participant. This is a simple way to verify your status.

Use Online Account Access

Many retirement plans offer online portals. Log in to your account to view your contributions. Check your participation summary or status there. It provides up-to-date information on your plan activity.

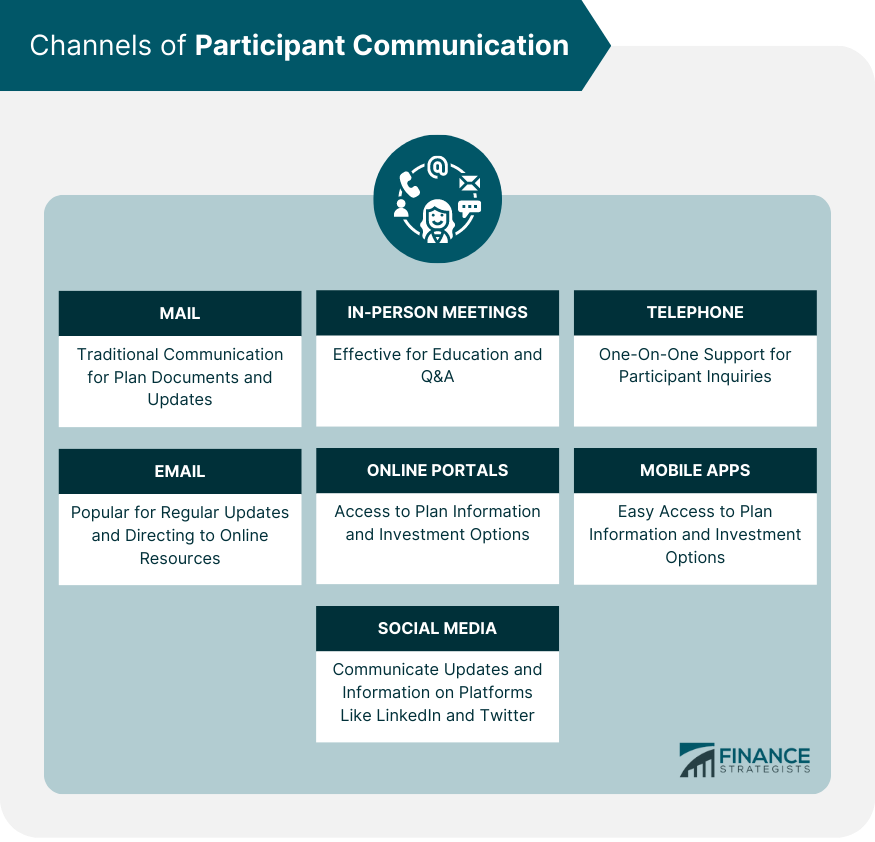

Credit: www.financestrategists.com

Frequently Asked Questions

What Is An Active Participant In A Retirement Plan?

An active participant is someone currently contributing or receiving benefits from a retirement plan.

How Does Active Participation Affect Retirement Benefits?

Active participants may have different benefit limits and tax rules compared to non-participants.

Can Part-time Workers Be Active Participants?

Yes, part-time workers can be active participants if they meet the plan’s eligibility rules.

Why Is Knowing Active Participant Status Important?

It helps understand contribution limits, tax rules, and plan eligibility for retirement savings.

How Does Active Participant Status Impact Tax Deductions?

Active participants may have lower tax deduction limits on retirement contributions than non-participants.

Conclusion

Understanding the role of an active participant helps you plan better. It shows who can contribute and benefit in retirement plans. Knowing this term can protect your future savings. Employers and employees both play important parts here. Keep learning about your retirement options and rules.

This knowledge leads to smarter decisions for your money. Stay informed and take control of your retirement journey. Planning early makes a big difference in the end.

Are you ready to secure your financial future with confidence? Understanding the Fairfax County Retirement Plan is a key step toward making your retirement years comfortable and stress-free. Whether you’re just starting your career or nearing retirement, knowing how this plan works can help you maximize your benefits and take control of your savings. You’ll…

Are you serving or have served in the military and wondering how your unique benefits affect your retirement? Your military service is more than just a job—it’s a powerful financial differentiator that can shape your retirement planning in ways many overlook. Understanding how to use these special advantages can secure your future and give you…

Are you a retired teacher in Texas looking for a dental plan that truly fits your needs? Taking care of your smile is important, especially after years of hard work in the classroom. But finding the right dental coverage can be confusing and overwhelming. That’s where the Texas Retired Teachers Dental Plan comes in. It’s…

Are you ready to take control of your financial future? The Illinois Retirement Plan Mandate is changing the way you and your employees save for retirement. Whether you’re a business owner or an employee, understanding this new rule is crucial. It affects your paycheck, your savings, and your peace of mind. Keep reading to discover…

Are you worried that the traditional retirement plans won’t give you the financial freedom you deserve? You’re not alone. Many people are looking for smarter, more flexible ways to secure their future. What if there was an alternative retirement plan that fits your unique needs and goals? You’ll discover options that could change the way…

Are you looking for a retirement plan that offers security and growth for your future? The Great Eastern Retirement Plan might be the solution you need. Understanding how this plan works can help you make smarter choices with your money. In this review, you’ll discover the key benefits, potential drawbacks, and what sets this plan…