Choosing the right retirement plan can feel overwhelming. You want to secure your future, but with so many options, how do you know which one fits your unique situation?

This guide will help you cut through the confusion and find the most advantageous retirement plan for you. By understanding your needs and goals, you’ll gain confidence in making choices that protect your financial freedom. Keep reading to discover the key factors that can make a real difference in your retirement strategy.

Types Of Retirement Plans

Choosing the right retirement plan can shape your financial future. Different plans suit different needs and jobs. Understanding the main types helps you pick what fits best. Each plan has unique features, benefits, and rules. Knowing these can save money and stress later.

Employer-sponsored Plans

These plans come from your workplace. The most common are 401(k) and 403(b) plans. You put money from your paycheck into the plan. Often, the employer adds money too, called a match. Taxes on the money can wait until you withdraw it. This plan helps you save without much effort.

Individual Retirement Accounts

IRAs are personal savings accounts for retirement. You open one yourself, not through work. Traditional IRAs let you delay taxes until retirement. Roth IRAs use after-tax money but offer tax-free withdrawals later. IRAs offer more control over investments. They work well if you do not have an employer plan.

Government Retirement Options

These plans are for public workers and certain professions. Examples include Social Security and military pensions. Social Security pays monthly benefits based on your work history. Some government jobs offer pensions, a steady income in retirement. These plans provide a reliable income source after you stop working.

Factors Influencing Plan Choice

Choosing the right retirement plan depends on many factors. These factors help decide which plan offers the best benefits. Understanding them makes planning easier and more effective.

Age And Time Horizon

Your age and how long you have until retirement matter a lot. Younger people can take more risks with investments. They have time to grow their money. Older individuals might prefer safer options. Time affects how much you can save and invest.

Income Level And Tax Bracket

Your income level impacts which plan suits you best. Higher earners might benefit from plans with tax breaks. Lower earners may want plans with immediate tax relief. Knowing your tax bracket helps choose the most cost-effective option.

Employment Status

Your job type influences available retirement plans. Employees often have access to employer-sponsored plans. Self-employed people might need to find individual plans. Retirees or unemployed individuals should consider options with flexibility.

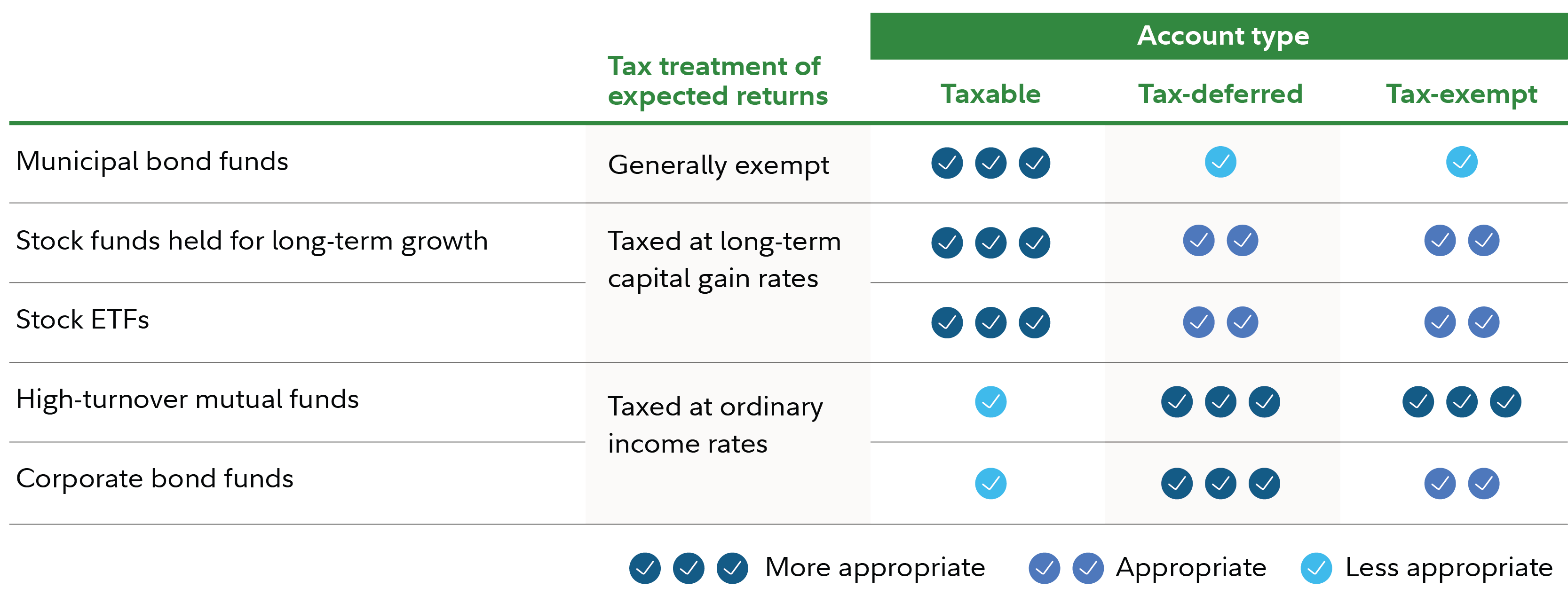

Comparing Tax Benefits

Choosing the right retirement plan depends on many factors. One key factor is the tax benefits each plan offers. Different plans have different ways of handling taxes. Understanding these differences helps you pick the best plan for your needs.

Tax-deferred Growth

Tax-deferred growth means your money grows without paying taxes each year. Taxes are paid later, usually at withdrawal. This allows your savings to grow faster over time. Many retirement plans offer this benefit. It helps your investments compound without yearly tax cuts.

Tax-free Withdrawals

Some plans let you take money out tax-free in retirement. You pay taxes on contributions, but not on withdrawals. This can save you money if tax rates rise later. It also provides predictable income after retirement. Tax-free withdrawals make budgeting easier for many retirees.

Tax Deductibility Of Contributions

Certain retirement plans let you deduct your contributions from taxable income. This lowers your tax bill during working years. It can put more money back in your pocket each year. Deductible contributions are a good way to reduce current taxes while saving for retirement.

Credit: www.ccu.com

Risk Tolerance And Investment Options

Choosing the right retirement plan involves understanding your risk tolerance and investment options. Risk tolerance means how much financial risk you are willing to accept. This affects the types of investments you should select. Some people prefer safer investments with steady returns. Others accept higher risks for the chance of bigger rewards. Knowing your comfort level with risk helps you pick the best plan. Investment options vary widely. They range from low-risk bonds to high-risk stocks. Each option fits different risk tolerances and retirement goals.

Conservative Vs Aggressive Strategies

Conservative strategies focus on protecting your money. They use safer investments like government bonds or fixed deposits. These grow slowly but steadily. They suit people who want to avoid big losses.

Aggressive strategies aim for higher growth. They invest in stocks or mutual funds with higher risk. These can bring bigger rewards but also bigger losses. They fit those who can handle market ups and downs.

Plan Investment Flexibility

Some retirement plans offer flexible investment choices. You can change your investments as your needs change. This helps you adjust risk levels over time. Other plans have limited options and less control.

Flexible plans allow shifting from aggressive to conservative strategies. This works well as you get closer to retirement. Plans with less flexibility may not suit all investors. Choose a plan that matches your risk comfort and control needs.

Withdrawal Rules And Penalties

Withdrawal rules and penalties shape how you use your retirement savings. They protect your funds for future use. Breaking these rules often leads to penalties. Knowing these rules helps you pick the best plan for your needs.

Required Minimum Distributions

Retirement plans require you to take out money at a certain age. This is called Required Minimum Distributions (RMDs). The IRS sets the age and amount you must withdraw. Missing RMDs can cause steep fines. These withdrawals ensure money is spent during retirement, not saved forever.

Early Withdrawal Consequences

Withdrawing money before the allowed age usually brings penalties. Many plans charge a 10% tax penalty on early withdrawals. You may also owe income taxes on the amount taken out. Some plans have exceptions, like disability or first home purchase. Early withdrawals reduce your future retirement savings and growth.

Maximizing Employer Contributions

Employer contributions can boost your retirement savings significantly. Many companies add money to your retirement plan as a benefit. Understanding how to maximize these contributions helps you grow your nest egg faster.

Knowing the rules and options around employer contributions lets you make smart choices. You can increase your total savings without extra effort or risk. This section explains key strategies and terms to watch for.

Matching Contributions Strategies

Matching contributions mean your employer adds money based on what you save. For example, they might match 50 cents for every dollar you put in. This match usually has a limit, like 5% of your salary.

To get the full match, contribute at least the amount your employer matches. Not doing this means missing free money. Some companies offer different match levels or special rules. Check your plan details carefully.

Vesting Schedules

Vesting refers to the time you must work before owning employer contributions fully. Until you are vested, you might lose some or all of these funds if you leave the job.

Vesting schedules vary. Some plans vest immediately. Others take years. Knowing your vesting timeline helps plan your career and retirement savings. It shows how long to stay to keep all employer money.

Tailoring Plans To Life Stages

Choosing the right retirement plan depends on your current life stage. Different plans fit different ages and financial goals. Tailoring your retirement plan helps you save smarter and prepare better. Each stage has unique needs and opportunities.

Young Professionals

Young professionals have time on their side. They can take more risks with investments. A plan with higher growth potential suits them well. Starting early means small amounts grow significantly. Focus on building good saving habits now.

Mid-career Savers

Mid-career savers may face more expenses and responsibilities. They need balanced plans that reduce risk but still grow. Increasing contributions is smart at this stage. Plans with tax benefits help maximize savings. Adjusting investments to be safer is wise.

Pre-retirees

Pre-retirees should protect their savings from big losses. Low-risk plans and steady income options work best. It is time to plan for withdrawal and taxes. Making sure funds are easy to access is important. Focus shifts from growth to security and stability.

Credit: www.business.com

Credit: www.fidelity.com

Frequently Asked Questions

What Factors Affect Choosing The Best Retirement Plan?

Income, job type, tax benefits, and retirement goals affect plan choice significantly.

How Does Age Influence Retirement Plan Decisions?

Younger people benefit from growth-focused plans; older individuals prefer stability and withdrawals.

Which Retirement Plan Suits Self-employed Individuals Best?

Solo 401(k) and SEP IRAs offer flexible contributions and tax advantages for self-employed workers.

Can Combining Retirement Plans Improve Savings?

Yes, combining plans like 401(k) and IRAs can boost savings and offer tax benefits.

Conclusion

Choosing the right retirement plan depends on your unique needs. Consider your income, goals, and risk comfort. Different plans suit different people and situations. Take time to compare options carefully. This helps secure your financial future better. Start planning early to get the most benefit.

Small steps now can make a big difference later. Keep learning and adjust your plan as life changes. Your retirement should feel safe and comfortable. Make informed choices to enjoy peace of mind.

Are you confident that your future is financially secure after you retire? Understanding your corporate retirement plan and fund is the key to making sure you have enough money when you stop working. This isn’t just about saving—it’s about knowing how your plan works, what benefits you can expect, and how to make smart choices…

Choosing the best Medicare for Retired Military, Medicare plan after your military service can feel overwhelming. You’ve dedicated years to serving your country, and now it’s time to make sure your healthcare matches the care you deserve. What if you could find a Medicare option designed to fit your unique needs as a retired military…

Plan your retirement with confidence. Discover the best retirement plans in the USA for 2026 — 401(k), IRA, Roth IRA, and more. Simple tips for Americans 50+ years. The best retirement plans in the USA include the 401(k), Traditional IRA, Roth IRA, SEP IRA, and Solo 401(k). The right plan depends on your age, income,…

Are you ready to secure your financial future with confidence? Understanding the Fairfax County Retirement Plan is a key step toward making your retirement years comfortable and stress-free. Whether you’re just starting your career or nearing retirement, knowing how this plan works can help you maximize your benefits and take control of your savings. You’ll…

Are you confused about the difference between a pension plan and a retirement plan? You’re not alone. Choosing the right option can shape how comfortable your future feels. Understanding these two can help you take control of your financial security and enjoy your golden years without stress. Keep reading to discover which plan suits your…

Are you looking for a retirement plan that offers security and growth for your future? The Great Eastern Retirement Plan might be the solution you need. Understanding how this plan works can help you make smarter choices with your money. In this review, you’ll discover the key benefits, potential drawbacks, and what sets this plan…