Best Teacher Retirement Plans by State: Top Picks for Secure Futures

Are you a teacher wondering how to secure your future after years of hard work? Choosing the right retirement plan can make all the difference in enjoying a comfortable and stress-free retirement.

But with so many options available, how do you know which plan works best for you, especially since benefits vary by state? This guide breaks down the best teacher retirement plans by state, helping you find the perfect fit for your needs.

Keep reading to discover how to make your retirement dreams a reality—because you deserve the best.

Credit: www.youtube.com

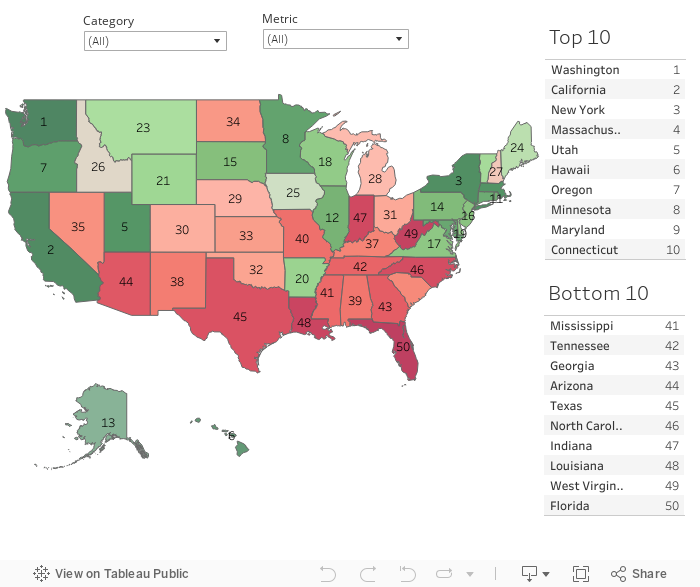

State-by-state Plan Comparison

Teacher retirement plans vary widely across the United States. Each state offers different benefits, rules, and options. Understanding these differences helps teachers plan better for their future. This section compares key features of teacher retirement plans by state. Some states offer defined benefit plans. These plans provide a fixed monthly payment after retirement. Other states use hybrid plans, mixing fixed benefits with personal savings accounts. Contribution rates, vesting periods, and retirement age also differ. These factors affect how much teachers receive later. Knowing how states compare helps teachers choose the best plan for their needs. It also guides those who might move between states during their careers.

Contribution Rates By State

Contribution rates show how much teachers must pay from their salary. Rates vary from around 6% to over 11%. Higher rates may mean better benefits later. Some states require both teachers and employers to contribute.

Vesting Periods Explained

Vesting means how long a teacher must work before earning full benefits. Most states require between 5 and 10 years. Shorter vesting periods offer quicker access to retirement funds. Longer periods encourage teachers to stay in the system.

Retirement Age Requirements

Retirement age rules differ by state and plan type. Many states set the minimum age between 55 and 62. Some allow earlier retirement with reduced benefits. Others require reaching a certain age plus years of service.

Benefit Calculations

States calculate retirement benefits using salary and years worked. A common formula multiplies years of service by a percentage of final salary. Some states use the highest average salary over several years. Benefit amounts vary widely by state.

Options For Early Retirement

Early retirement options depend on state rules. Some states let teachers retire early with smaller payments. Others require a minimum number of service years before early retirement. Penalties or reduced benefits often apply.

Key Features Of Top Plans

Teacher retirement plans vary by state but share important features. These features protect your future and offer financial support after years of teaching. Understanding these key elements helps you choose a solid plan. Each top plan includes benefits designed for educators. They focus on security, flexibility, and clear rules. Knowing what to expect can ease your retirement planning.

Guaranteed Pension Benefits

Most top plans offer a fixed monthly pension. This pension depends on your years of service and final salary. It provides steady income and peace of mind after retirement.

Cost-of-living Adjustments (cola)

Many states adjust pensions yearly for inflation. This protects your purchasing power over time. COLA helps your retirement income keep up with rising costs.

Health Insurance Options

Some plans include health benefits or subsidies. These lower your medical costs during retirement. Health coverage is a key feature for many retired teachers.

Vesting Periods

Vesting means you earn the right to a pension after working a set time. Most states require 5 to 10 years. Knowing the vesting period helps you plan your career path.

Disability And Survivor Benefits

Top plans offer protection if you become disabled or pass away. Benefits may continue for your family or cover medical needs. This adds financial security beyond retirement.

Optional Contribution Plans

Some states allow extra contributions to boost retirement savings. These voluntary plans increase your final benefits. They offer more control over your retirement income.

Benefits And Payout Structures

Teacher retirement plans vary by state, especially in benefits and payout structures. These elements shape how much teachers receive after retirement and how long payments last. Understanding these details helps teachers plan their future better. Benefits often include monthly payments, survivor benefits, and cost-of-living adjustments. Payout structures define how payments are calculated and distributed over time. Both factors impact financial security during retirement.

Monthly Pension Payments

Most teacher retirement plans offer monthly pension payments. These payments depend on years of service and average salary. Some states use a formula to calculate the exact amount. Payments continue for the retiree’s lifetime.

Cost-of-living Adjustments (cola)

Many plans include cost-of-living adjustments. COLA helps pensions keep up with inflation. Not all states offer COLA, and amounts vary widely. This feature protects retired teachers’ buying power over time.

Survivor And Disability Benefits

Retirement plans often provide survivor benefits for spouses or dependents. Disability benefits may also be part of the package. These benefits offer extra security in case of unexpected events.

Optional Lump-sum Payments

Some states allow retirees to choose lump-sum payments. This option lets teachers receive a one-time payment instead of monthly checks. It suits those who prefer a large sum upfront.

Vesting Periods And Eligibility

Vesting periods determine when teachers qualify for benefits. Usually, a minimum number of years of service is required. Early retirement may reduce monthly payments or benefits. Knowing these rules helps plan retirement timing.

Contribution Requirements

Contribution requirements are a key part of teacher retirement plans. They determine how much teachers must pay into their pension funds. These rules vary widely by state and impact retirement savings. Understanding contribution rules helps teachers plan better for their future. Some states require fixed percentages from salaries. Others have flexible or tiered systems based on years of service.

Employee Contribution Rates

Most states ask teachers to contribute a portion of their salary. Rates typically range between 6% and 12%. Some states have flat rates, while others use sliding scales. Higher rates can mean larger benefits later. Lower rates may allow more take-home pay now. Teachers should check their state’s specific rate.

Employer Contribution Obligations

States or school districts also contribute to teacher retirement plans. Employer contributions often match or exceed employee payments. This boosts the total retirement fund balance. The exact amount depends on state laws and funding health. Some states adjust employer contributions annually based on pension needs.

Vesting Periods And Contribution Effects

Vesting means earning the right to retirement benefits. Contribution periods usually affect vesting time. Teachers may need to contribute for 5 to 10 years before benefits become guaranteed. Leaving before vesting can reduce or eliminate pension payouts. Understanding vesting helps teachers make informed career choices.

Investment Options And Flexibility

Investment options and flexibility are key to a strong teacher retirement plan. These features help teachers control their savings and adapt to life changes. A good plan offers a range of choices and easy adjustments. This way, teachers can build a secure future.

Types Of Investment Options

Most teacher retirement plans include stocks, bonds, and mutual funds. Some states offer target-date funds that adjust risk over time. Others provide stable value funds for steady growth. Diversity helps manage risks and rewards. Teachers can pick options that fit their needs and goals.

Plan Flexibility And Control

Plans vary in how much control teachers have over investments. Some allow changing investments anytime. Others limit changes to certain periods. Flexibility helps teachers respond to market changes and personal situations. It also lets them rebalance their portfolios easily.

Automatic Features And Customization

Many plans include automatic features like contribution increases. This helps teachers save more over time without extra effort. Some plans offer personalized advice to guide investment choices. Custom options support teachers at different career stages and risk levels.

Credit: www.reddit.com

Retirement Age And Eligibility

Teacher retirement plans vary widely by state. One key factor is the retirement age and eligibility rules. These rules determine when teachers can retire and receive benefits. Understanding these rules helps teachers plan their future better. Each state sets its own retirement age. Some states allow early retirement with reduced benefits. Others require teachers to work longer for full benefits. Eligibility often depends on years of service and age.

Minimum Retirement Age Requirements

States set a minimum age for teacher retirement. This age usually ranges from 55 to 65 years. Some states allow retirement as early as 50 with enough service years. Others have stricter age limits to qualify for full benefits.

Years Of Service Needed For Eligibility

Most states require teachers to work a certain number of years. Common requirements range from 20 to 30 years of service. Teachers with fewer years may retire early but get smaller pensions. Full benefits usually need both age and service requirements met.

Early Retirement Options And Penalties

Early retirement is possible in many states. It often carries a penalty, lowering monthly payments. Penalties reduce pension amounts by a small percent for each year early. Some states offer special programs for early retirement without penalties.

Exceptions And Special Cases

Certain states have exceptions for disability or military service. Teachers in hazardous roles may retire earlier. Some states provide benefits for part-time or substitute teachers. Rules vary greatly, so checking specific state laws is important.

Additional Perks And Support

Teacher retirement plans often offer more than just a pension. States provide extra benefits and support to help retired teachers enjoy their retirement years. These perks can include healthcare options, financial counseling, and special discounts. Such support makes retirement smoother and less stressful. Understanding these additional benefits is key to choosing the best retirement plan. They add real value beyond monthly payments. Each state’s offerings vary, so knowing what is available helps teachers plan better.

Healthcare Benefits After Retirement

Many states offer retired teachers access to health insurance. Some plans cover medical, dental, and vision care. These benefits reduce out-of-pocket costs for retirees. Affordable healthcare is crucial for a comfortable retirement.

Financial Planning And Counseling Services

States often provide free or low-cost financial advice. This guidance helps teachers manage their retirement funds wisely. Counseling may include budgeting, investment tips, and tax planning. Good advice can protect savings and increase financial security.

Discounts And Special Offers For Retired Teachers

Retired teachers receive discounts on various services and products. These can include travel, entertainment, and retail stores. Discounts help stretch retirement income further. Many states promote these offers as a thank you to educators.

Credit: scholaroo.com

Frequently Asked Questions

What Are The Best Teacher Retirement Plans By State?

Teacher retirement plans vary by state, offering different benefits like pensions and 401(k) options.

How Do Teacher Pensions Differ Across States?

States differ in pension amounts, eligibility rules, and contribution rates for teachers.

Can Teachers Access Retirement Funds Early Without Penalty?

Some states allow early access under specific conditions, but penalties often apply.

Are 401(k) Plans Available For Public School Teachers?

Many states offer 401(k) or similar plans alongside pensions for extra savings.

How Does Cost Of Living Affect Teacher Retirement Benefits?

Higher cost of living states may offer larger pensions to help maintain lifestyle.

Conclusion

Teacher retirement plans differ widely across states. Each plan offers unique benefits and rules. Understanding these differences helps teachers choose wisely. Planning early secures a comfortable retirement. State options may include pensions, savings, or hybrid plans. Teachers should review their state’s specific retirement details.

Knowledge about plans leads to better financial decisions. Secure retirement starts with informed choices today.